I’ll admit it: There are times that I think everything that needs to be said about personal finance has been said already, that all of the information is out there just waiting for people to find it. The problem is solved.

Perhaps this is technically true, but now and then — as this morning — I’m reminded that teaching people about money is a never-ending process. There aren’t a lot of new topics to write about, that’s true (this is something that even famous professional financial journalists grouse about in private), but there are tons of new people to reach, people who have never been exposed to these ideas. And, more importantly, there’s a constant stream of new misinformation polluting the pool of smart advice. (Sometimes this misinformation is well-meaning; sometimes it’s not.)

Here’s an example. This morning, I read a piece at Slate by Felix Salmon called “The Millionaire’s Mortgage”. Salmon’s argument is simple: “Paying off your house is saving for retirement.”

Now, I don’t necessarily disagree with this basic premise. I too believe that money you pay toward your mortgage principle is, in effect, money you’ve saved, just as if you’d put it in the bank or invested in a mutual fund. Many financial advisers say the same thing: Money you put toward debt reduction is the same as money you’ve invested. (Obviously, they’re not exactly the same but they’re close enough.)

So, yes, paying off your home is saving for retirement. Or, more precisely, it’s building your net worth.

But aside from a sound basic premise, the rest of Salmon’s article boils down to bullshit.

Lying with Statistics

Looking past the “paying off your house is saving for retirement” subtitle on his piece (a subtitle that was likely added by an editor, not by Salmon), we get to his actual thesis: “Making mortgage payments can, in theory, be a way to accumulate wealth almost as effectively as contributing to a retirement fund.”

I’m glad Salmon qualified this statement with “in theory” and “almost” because this is pure unadulterated bullshit. And it’s dangerous bullshit. Here’s how this “logic” works:

If you buy an urban house today for $315,000 (the average price) and it appreciates at 8 percent a year for the next 15 years, you will be living in a $1 million house by the time you pay off your 15-year mortgage, and you will own it free and clear. Which is to say: You’ll be a millionaire.

For this to be true, here’s what has to happen.:

Home prices in your area have to appreciate at an average of eight percent not just this year and next year, but for fifteen years.

You have to take out a 15-year mortgage instead of a 30-year mortgage.

You need to stay in that house (or continue to own it) for that entire fifteen years.

Once you’ve become a millionaire homeowner, you now have to tap that equity for it to be of use. To do that, you have to sell your home, acquire a reverse mortgage, or otherwise creatively access the value locked in your home.

The real problem here, of course, are the assumptions about real estate returns. Salmon spouts huckster-level nonsense:

The 8 percent appreciation rate is aggressive, but not entirely unrealistic: It’s lower than the 8.3 percent appreciation rate from 2011 through 2017, and also lower than the 9 percent appreciation rate from 1996 to 2007.

That’s right. Salmon cites stats from 1996 to 2007, then 2011 to 2017 — and completely leaves out 2008 to 2010. WTF?

This as if I ran a marathon and told you that I averaged four minutes per mile…but I was only counting the miles during which I was running downhill! Or I told you that Get Rich Slowly earned $5000 per month…but I was only giving you the numbers from April. Or I logged my alcohol consumption for thirty days and told you I averaged three drinks per week…but left out how much I drank on weekends.

This isn’t how statistics work! You don’t get to cherry pick the data. You can’t just say, “Homes in some markets appreciated 9% annually from 1996 to 2007, then 8.3% annually from 2011 to 2017. Therefor, your home should increase in value an average of eight percent per year.” What about the gap years? What about the period before the (very short) 22 years you’re citing? What makes you think that the boom times for housing are going to continue?

Long-Term Home Price Appreciation

In May, I shared a brief history of U.S. homeownership. To write that article, I spent hours reading research papers and sorting through data. One key piece of that post was the info on U.S. housing prices.

Let me share that info again.

For 25 years, Yale economics professor Robert Shiller has tracked U.S. home prices. He monitors current prices, yes, but he’s also researched historical prices. He’s gathered all of this info into a spreadsheet, which he updates regularly and makes freely available on his website.

This graph of Shiller’s data (through January 2016) shows how housing prices have changed over time:

Shiller’s index is inflation-adjusted and based on sale prices of existing homes (not new construction). It uses 1890 as an arbitrary benchmark, which is assigned a value of 100. (To me, 110 looks like baseline normal. Maybe 1890 was a down year?)

As you can see, home prices bounced around until the mid 1910s, at which point they dropped sharply. This decline was due largely to new mass-production techniques, which lowered the cost of building a home. (For thirty years, you could order your home from Sears!) Prices didn’t recover until the conclusion of World War II and the coming of the G.I. Bill. From the 1950s until the mid-1990s, home prices hovered around 110 on the Shiller scale.

For the past twenty years, the U.S. housing market has been a wild ride. We experienced an enormous bubble (and its aftermath) during the late 2000s. It looks very much like we’re at the front end of another bubble today. As of December 2017, home prices were at about 170 on the Shiller scale. (Personally, I believe that once interest rates begin to rise again, home prices will decline.)

Here’s the reality of residential real estate: Generally speaking, home values increase at roughly the same (or slightly more) than inflation. I’ve noted in the past that gold provides a long-term real return of roughly 1%, meaning that it outpaces inflation by 1% over periods measured in decades. For myself, that’s the figure I use for home values too.

Crunching the Numbers

Because I’m a dedicated blogger (or dumb), I spent an hour building this chart for you folks. I took the afore-mentioned housing data from Robert Shiller’s spreadsheet and combined it with the inflation-adjusted closing value of the Down Jones Industrial Average for each year since 1921. (I got the stock-market data here.) If you’d like, you can click the graph to see a larger version.

Let me explain what you’re seeing.

First, I normalized everything to 1921. That means I set home values in 1921 to 100 and I set the closing Down Jones Industrial Average to 100. From there, everything moves as normal relative to those values.

Second, I’m not sure why but Excel stacked the graphs. (I’m not spreadsheet savvy enough to fix this.) They should both start at 100 in 1921, but instead the stock market graph starts at 200. This doesn’t really make much of a difference to my point, but it bugs me. There are a few places — 1932, 1947 — where the line for home values should actually overtake the line for the stock market, but you can’t tell that with the stacked graph.

As the chart shows, the stock market has vastly outperformed the housing market over the long term. There’s no contest. The blue housing portion of my chart is equivalent to the line in Shiller’s chart (from 1921 on, obviously).

Now, having said that, there are some things that I can see in my spreadsheet numbers that don’t show up in this graph.

Because Felix Salmon at Slate is using a 15-year window for his argument, I calculated 15-year changes for both home prices and stock prices. I’ll admit that the results surprised me. Generally speaking, the stock market does provide better returns than homeownership. However, in 30 of the 82 fifteen-year periods since 1921, housing provided better returns. (And in 14 of 67 thirty-year periods, housing was the winner.) I didn’t expect that.

In each of these cases, housing outperformed stocks after a market crash. During any 15-year period starting in 1926 and ending in 1939 (except 1932), for instance, housing was the better bet. Same with 1958 to 1973. In other words, if you were to buy only when the market is declining, housing is probably the best bet — if you’re making a lump-sum investment and not contributing right along.

Another thing the numbers show is that you’re much less likely to suffer long-term declines with housing than with the stock market. Sure, there are occasional periods where home prices will drop over fifteen or thirty years, but generally homes gradually grow in value over time.

The bottom line? I think it’s perfectly fair to call your home an investment, but it’s more like a store of value than a way to grow your wealth. And it’s nothing like investing in the U.S. stock market.

Honestly, I probably would have ignored Salmon’s article if it weren’t for the attacks he makes on saving for retirement. Take a look at this:

If you’re the kind of person who can max out your 401(k) every year for 30 or 40 years straight — disciplined, frugal, and apparently immune to misfortune — then, well, congratulations on your great good luck, and I hope you’re at least a little bit embarrassed at how much of a tax break you’re getting compared to people who need government support much more than you do.

Holy cats! Salmon has just equated the discipline and frugality that readers like you exhibit with “good luck”, and simultaneously argued that you should be embarrassed for preparing for your future. He wants you to feel guilty because you’re being proactive to prepare for retirement. Instead of doing that, he wants you to buy into his bullshit “millionaire’s mortgage” plan.

This crosses the line from marginal advice to outright stupidity.

There’s an ongoing discussion in the Early Retirement community about whether or not you should include home equity when calculating how much you’ve saved for retirement. There are those who argue “absolutely not”, you should never consider home equity. (A few of these folks don’t even include home equity when computing their net worth, but that fundamentally misses the point of what net worth is.)

I come down on the other side. I think it’s fine — good, even — to include home equity when making retirement calculations. But when you do, you need to be aware that the money you have in your home is only accessible if you sell or use the home as collateral on a loan.

Regardless, I’ve never heard anyone in the community argue that you ought to use your home as your primary source of retirement saving instead of investing in mutual funds and/or rental rental properties. You know why? Because it’s a bad idea!

I read a lot of books. Nearly every book has some nugget of wisdom I can take from it, but it’s rare indeed when I read a book and feel like I’ve hit the mother lode. In 2018, I’ve been fortunate enough to read two books that I’ll be mining for years to come.

The first was Sapiens, the 2015 “brief history of mankind” from Yuval Noah Harari. I finished the second book yesterday: Thinking in Bets by Annie Duke. Duke is a professional poker player; Thinking in Bets is her attempt to take lessons from the world of poker and apply them to making smarter decisions in all aspects of life.

“Thinking in bets starts with recognizing that there are exactly two things that determine how our lives turn out,” Duke writes in the book’s introduction. Those two things? The quality of our decisions and luck. “Learning to recognize the difference between the two is what thinking in bets is all about.”

We have complete control over the quality of our decisions but we have little (or no) control over luck.

The Quality of Our Decisions

The first (and greatest) variable in how our lives turn out is the quality of our decisions.

People have a natural tendency to conflate the quality of a decision with the quality of its outcome. They’re not the same thing. You can make a smart, rational choice but still get poor results. That doesn’t mean you should have made a different choice; it simply means that other factors (such as luck) influenced the results.

Driving home drunk, for instance, is a poor decision. Just because you make arrive home without killing yourself or anyone else does not mean you made a good choice. It merely means you got a good result.

Duke gives an example from professional football. At the end of Super Bowl XLIX, the Seattle Seahawks were down by four points with 26 seconds left in the game. They had the ball with second down at the New England Patriots’ one-yard line. While everbody expected them to run the ball, they threw a pass. That pass was intercepted and the Seawhawks lost the game.

Armchair quarterbacks around the world complained that this was the worstplay-call in NFLhistory. (I’ve linked to just four stories there. They’re all brutal. You can find many more online.)

Duke argues, though, that the call was fine. In fact, she believes it was a smart call. It was a quality decision. There was only a 2% chance that the ball would be intercepted. There was a high percentage chance of winning the game with a touchdown. Most importantly, if the pass was incomplete, the Seahawks would have two more plays to try again. But if the team opted to run instead? Because they only had one time-out remaining, they’d only get one more chance to score if they failed.

The call wasn’t bad. The result was bad. There’s a big difference between these two things, but humans generally fail to differentiate between actions and results. Duke says that poker players have a term for this logical fallacy: “resulting”. Resulting is assuming your decision-making is good or bad based on a small set of outcomes.

If you play your cards correctly but still lose a hand, you’re “resulting” when you focus on the outcome instead of the quality of your decisions. You cannot control outcomes; you can only control your actions.

Note: As long-time readers know, I grew up Mormon. One of the songs we were taught as children has this terrific lyric: “Do what is right, let the consequence follow.” This has become something of a mantra for me as an adult. If I do the right thing — whatever that might be in a given context — then I cannot feel guilty if I get a poor result. It’s my job to do my best. Beyond that, I cannot control what happens.

Luck and Incomplete Information

Why don’t smart decisions always lead to good results? Because we don’t have complete control over our lives — and we don’t have all of the information. Fundamentally, Duke says, results are influenced by luck. Randomness. Chance. Happenstance. She writes:

“We are uncomfortable with the idea that luck plays a significant role in our lives. We recognize the existence of luck, but we resist the idea that, despite our best efforts, things might not work out the way we want. It feels better to imagine the world as an orderly place, where randomness does not wreak havoc and things are perfectly predictable.”

Duke contrasts poker (and life) with chess. Chess is a game of complete information, a game of pure skill. There’s no luck involved. At all times, all of the pieces are available for both players to see. There are no dice rolls, nothing to randomize the game. As a result, the better player almost always wins. (When the better player doesn’t win, it’s because of easily identifiable mistakes.) Because chess is a game of complete information, luck isn’t a factor — the outcome is only a matter of the quality of your decisions.

In poker, however, there’s a lot you don’t know. What cards do your opponents hold? What cards remain in the deck? How likely are your opponents to bluff? And so on. Experienced poker players learn to think in terms of odds. “With this hand, I have a 74% chance of winning.” “I should fold. These cards only give me a 18% chance of coming out ahead.”

It’s because our decisions are made with incomplete information that life sometimes seems so difficult. You can do the right thing and still get poor results. You can opt not to drink on New Year’s Eve, for instance, but still get blindsided by somebody who did to drink and drive. You made a quality decision, but happenstance hit you upside the head anyhow.

Duke cites a scene from The Princess Bride as an example of how incomplete information affects the outcomes of our decisions. Criminal mastermind Vizzini and the Dread Pirate Roberts engage in a battle of wits:

Vizzini pours two goblets of wine, then Roberts (actually our hero, Westley, in disguise) poisons one of them with deadly “ioacane powder”. The challenge is for Vizzini to choose the non-poisoned goblet. Vizzini cackles with glee when Roberts/Westley downs the poison — but then falls dead after drinking his own goblet. It turns out both goblets had been poisoned, but Roberts had spent the previous few years building an immunity to iocane powder.

Vizzini made a quality decision based on the information he had, but he didn’t have all of the information: both goblets were poisoned, and his opponent in this “battle of wits” was immune to the poison in the first place!

Thinking in Bets

Duke argues that in order to make smarter decisions, we have to embrace both the idea that there’s a lot of luck in life and the reality that we’re swimming in uncertainty. There’s a stigma in our culture about appearing ignorant, about being unsure. Duke says that becoming comfortable with uncertainty and not knowing is a vital step to becoming a better decision-maker.

“Admitting that we don’t know has an undeservedly bad reputation,” she writes.

“What makes a decision great is not that it has a great outcome. A great decision is the result of a good process, and that process must include an attempt to accurately represent our own state of knowledge. That state of knowledge, in turn, is some variation of ‘I’m not sure’.”

Duke suggests that by moving to a framework of “I’m not sure”, we’re far less likely to fall into the trap of black and white thinking, of false certainty. She cites Stuart Firestein’s TED talk about the pursuit of ignorance:

We should be pursuing “high-quality ignorance”.

Based on all of this, how then can we make smarter decisions? Duke says that we should stop thinking in terms of right and wrong. Few things are ever 0% or 100% likely to occur. Few people are ever 0% or 100% right about what they know or believe. Instead, we should think in bets.

“Decisions are bets on the future,” Duke writes, “and they aren’t ‘right’ or ‘wrong’ based on whether they turn out well on any particular iteration. An unwanted decision doesn’t make our decision wrong if we thought about the alternatives and probabilities in advance and allocated our resources accordingly.”

Duke says that because pro poker players learn to think in terms of odds during their games, they transfer this way of thinking to everyday life. “Job and relocation decisions are bets,” she writes. “Sales negotiations and contracts are bets. Buying a house is a bet. Ordering the chicken instead of the steak is a bet. Everything is a bet.”

Just as each poker bet carries a different chance of success (based on the quality of the hand, the hands of the other players, etc.), so too the bets we make in life carry different chances of success. And our personal beliefs have (or should have) varying degrees of certainty. Duke wants readers to begin thinking about their beliefs and decisions in terms of probabilities rather than in terms of black and white.

Turns out I already do this to a small degree — but usually for minor stuff. In fact, I’ve done it several times in the past week.

A few days ago, I was listening to a Big Band station on Pandora. The song “Green Eyes” came on. “I wonder what year this is from?” I thought. I listened to the vocals, to the band, to the recording quality. “I think there’s an 80% chance this song is from 1939 — give or take two years,” I thought. I looked it up. The song was released in 1941. (I listen to a lot of older music, and I play this game often.)

Because it’s been hot in Portland lately, folks in my neighborhood have all been taking early morning walks. We all tend to follow the same two-mile loop because it’s easy. I’ve started playing a game when I pass somebody. “Okay, the dog and I passed David Hedges at the llama farm. Where will we encounter him on the top side of the loop? I’ll be it’s between Roy’s house and the bottom of the hill.” It’s fun for me to see how accurate my guesses are.

Duke believes that we should each do this sort of thing whenever we make a decision. Before we commit to a course of action, we should think about possible outcomes and how likely each of those outcomes is to occur.

Let’s say you’ve only got $200 in the bank and it’s a week from payday. Should you join your friends for that weekend motorcycle trip? Or should you save that cash in case something goes wrong? Or, thinking farther in the future, what outcomes are you seeking in life? What decision will improve the odds of achieving those outcomes?

Or, imagine that you’re trying to decide whether or not to buy a home. As you consider the possibilities, think about the probability that each possible future will occur. Don’t simply cling to the outcome you’re hoping for. Be objective. If the odds of success seem reasonable, then pursue your desired course of action. But if they don’t, then pull the plug.

Duke writes:

“In most of our decisions, we are not betting against another person. Rather, we are betting against all the future versions of ourselves that we are not choosing. We are constantly deciding among alternative futures: one where we go to the movies, one where we go bowling, one where we stay home. Or futures where we take a job in Des Moines, stay at our current job, or take some time away from work. Whenever we make a choice, we are betting on a potential future.”

Every choice carries an opportunity cost. When you choose to save for the future, for instance, you’re giving up pleasure in the present. Or, if you choose to spend in the present, you’re giving up future financial freedom.

Final Thoughts

For a long time, I’ve argued that the best books about money are often not about money at all. Thinking in Bets is another example of this. While Duke uses plenty of personal finance examples, the book itself is about self-improvement. It’s not a money manual. Yet the info here could have a profound impact on your financial future.

There’s a lot more in this book that I haven’t covered in my review. (I’ve really only touched on the first third of the material!) For me, the biggest takeaway comes early: It’s vital to separate decision quality from results. The rest of the book explores how to improve the quality of your decisions.

Among the strategies Duke advocates are these:

Learn to examine your own beliefs. Be your own devil’s advocate. If you’re certain about something, explore the opposing viewpoint. (If you’re liberal, seek conservative opinions. If you’re conservative, look for liberal voices.) Be skeptical — of yourself and others.

Build a network of trusted advisors, people who can give you feedback on your beliefs and decisions. But don’t make these support groups homogeneous. Draw on people from a variety of backgrounds and belief systems. If you only associate with people who think the same way you do, you never give yourself a chance to grow, and you’ll never spot possible errors in your thinking. (This is like the current problems Facebook is facing with its deliberately-created echo chambers, which only serve to reinforce the way people think instead of challenging them.)

When you make decisions, think of the future. Use barriers and pre-commitment to do the right thing automatically. Practice backcasting, a visualization method in which you define a desired outcome then figure out how you might get there.

The book is dense — dense! — with ideas and information. When I finished it, I wanted to go back and read it again. Plus, I wanted to plow through the nearly 200 other works that Duke lists in her bibliography. I feel like I could spend an entire year diving deeper into this book and its related reading.

But, as much as I wish it were, Thinking in Bets isn’t perfect. A strong argument could be made that this material would work better as a TED talk or a 5000-word essay in The Atlantic (or on Get Rich Slowly!). The book is so packed with info that it sometimes loses its way. There’s also a lot of repetition — too much repetition. Plus, it seems to lack a clear sense of organization.

These quibbles aside, Thinking in Bets has earned a permanent place on my bookshelf. If I ever get around to putting together a Get Rich Slowly library (a project I’ve been planning for years!), this book will be in it. I got a lot out of it. And I bet you will too.

The 2018 edition of Can I Retire is now available (print edition here, Kindle edition here). That’s (finally) the last of the 2018 updates to reflect the new tax law. To be clear, the biggest change with this update is simply new tax information. So if you’ve read a prior edition, there’s probably not a lot to be gained from buying/reading the new edition as well.

For anybody who hasn’t yet read the book and is curious what’s in it, the table of contents is as follows:

Part One: How Much Money Will You Need to Retire?

1. How Much Income Will You Need?

Calculating your expenses

Adjusting for inflation

Adjusting for taxes

Adjusting for pensions, Social Security, and other income

2. Safe Withdrawal Rates: The 4% “Rule”

Why only 4%?

Volatility is bad news when selling.

Sequence of returns risk

It’s only a guideline.

3. What if 4% Isn’t Enough?

Possible options

Increasing returns isn’t easy.

4. Retirement Planning with Annuities

What is a SPIA?

Annuity income: Is it safe?

Minimizing your risk

5. How Much (and When) to Annuitize

Creating a safe floor

Annuitizing as a backup plan

Social Security as an annuity

Part Two: Managing a Retirement-Stage Portfolio

6. Asset Allocation in Retirement

Assessing your risk tolerance

There’s no “right” answer.

Stocks vs. bonds

Bond risk levers

Stock risk levers

Rebalancing your portfolio

7. Index funds and ETFs vs. Active Funds

8. 401(k) Rollovers

Reasons to roll over a 401(k)

Reasons not to roll over a 401(k)

How and where to roll over a 401(k)

Part Three: Tax Planning in Retirement

9. Roth Conversions

Roth conversions & retirement planning

How to execute a Roth conversion

Roth conversions of nondeductible contributions

10. Distribution Planning

Fill your 0% tax bracket

Taxable account before retirement accounts

Roth before tax-deferred?

Social Security: It’s complicated.

11. Asset Location

Tax-shelter your bonds

The role of interest rates

Tax-shelter your REITs

Foreign tax credit

Disclaimer:Your subscription to this blog does not create a CPA-client or other professional services relationship between you and Mike Piper or between you and Simple Subjects, LLC. By subscribing, you explicitly agree not to hold Mike Piper or Simple Subjects, LLC liable in any way for damages arising from decisions you make based on the information available herein. Neither Mike Piper nor Simple Subjects, LLC makes any warranty as to the accuracy of any information contained in this communication. I am not a financial or investment advisor, and the information contained herein is for informational and entertainment purposes only and does not constitute financial advice. On financial matters for which assistance is needed, I strongly urge you to meet with a professional advisor who (unlike me) has a professional relationship with you and who (again, unlike me) knows the relevant details of your situation.

You may unsubscribe at any time by clicking the link at the bottom of this email (or by removing this RSS feed from your feed reader if you have subscribed via a feed reader).

Yesterday at the Financial Careers forum on Reddit, a user named /u/unfoldcareers posted some useful advice for job-seekers. “ I’ve reviewed...

The poster notes that “bad resume format” leads most folks to get little or nor response to their job applications. To help current job hunters, /u/unfoldcareers created a free resume template that can be downloaded via Google Docs.

The Reddit post itself contains a number of useful tips. To craft a better resume, you should:

Be precise. Don’t speak in general terms, but include specific numbers and metrics. Instead of saying, “Was top salesperson at my company,” note how many people were on the sales team, how much better you performed than everybody else, and for how long.

Emphasize impact. According to /u/unfoldcareers, too many people focus on their achievements when they should really emphasize the impact they had on their company or team.

Stick to one page — unless you really do have decades of experience.

Make it scannable. “A hiring manager will review your resume for approximately 10 seconds or less,” writes /u/unfoldcareers. Be sure that they’ll be able to scan all of the important info quickly.

Explain gaps. Don’t leave a mystery. If you took time off to be a stay-at-home parent, say so.

Remove the “objective” line. It’s irrelevant. (I did a very little hiring for our family’s box factory. I never did understand why people put an objective on their resume.)

Remove references. It’s fine to create a separate document that contains your references so that you can provide them if asked, but don’t include them on the resume itself.

The full post on Reddit includes more info, of course, along with the reasoning behind some of the recommendations.

From my experience, most people forget is that a resume isn’t really about you. That might sound strange, but the truth is that a resume is about how well your skills and experience match an employer’s job requirements. Because of this, the best resumes are individually tailored to specific jobs.

Sure, you might create a “base” or “default” resume that serves as a framework when applying for work. But you’ll have greater success with your job hunt if you take the time to make subtle tweaks to this default each time you apply for a different job.

Also: I believe strongly that, whenever possible, you should hand-deliver your resume.

Obviously, this doesn’t work for online-only applications or for positions outside your local area. But I know that when we hired at the box factory, we paid more attention to folks who had come by in person than those who simply mailed their resume. (And from watching Kim go through a couple of job searches now, I’d say that one of the reasons she has such success is that she literally goes door to door, dropping her resume off at different dental offices.)

According to the article, there are three primary factors that determine “the adequacy of retirement resources”. Those are:

When a person begins participating in an employer-sponsored saving plan,

What percentage of their earnings they save in such a plan (i.e., their saving rate), and

At what age they retire and begin taking Social Security benefits.

Until Elon Musk invents a time submarine, it’s impossible for a worker to go back to their youth and begin saving for retirement earlier. Because of this, the authors focused their research on the relative power of saving more and working longer.

Note: To simplify matters, the authors make some assumptions. For instance, instead of investing in the highly-variable stock market, they assume their hypothetical subjects invest in a vehicle with a fixed rate of return: an annuity. This is a little goofy, but helps them come up with more precise numbers than they’d otherwise be able to achieve. Just keep this in mind as we talk about the article’s conclusions.

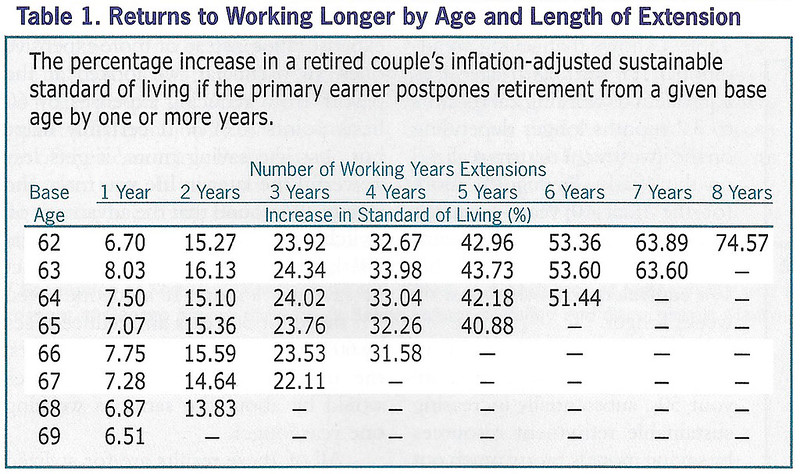

The Power of Working Longer

First, the authors look at what happens when a person decides to delay retirement by a year — or more. Generally speaking, each extra year worked brings roughly a 7.5% increase to standard of living during retirement. And that’s assuming a real (inflation-adjusted) investment return of 0%!

Here’s a table from the article that shows the potential increases in standard of living that come from delaying retirement. (All of these numbers assume 0% real returns.)

As you an see, if a 62-year-old opted to work an additional three years instead of retire, they’d enjoy an increased standard of living of nearly 24%. Working longer is a powerful way to increase your “retirement resources”.

The authors’ research found that while investment returns do have an effect on retirement standard of living, they’re not nearly as large as the effect of working longer. Assuming 0% real returns on investments, delaying retirement age from 66 to 67 leads to a 7.75% increase in standard of living. With a 7% real return (similar to average stock market returns), that one-year delay in retirement brings an increased standard of living of 9.56%. It’s a boost, yes, but not even a 2% boost over assuming zero investment returns.

The bottom line? Each extra year you work past your target retirement age brings a boost of roughly 10% to your post-retirement standard of living. Not too shabby.

The Power of Saving

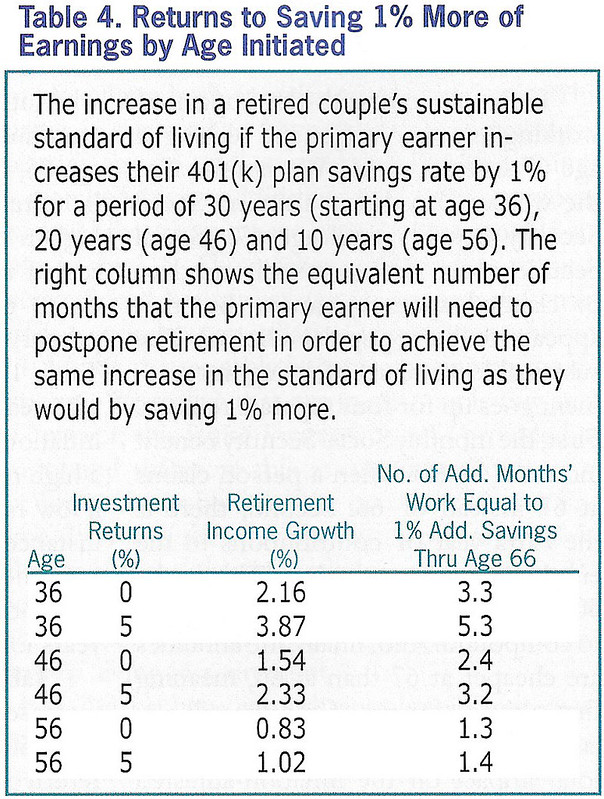

The real reason this article caught my eye was the authors’ discussion of saving. They dismiss saving rate as being less powerful than working longer, but I’m not sure that I agree. (Remember, I believe that your saving rate is the most important number in personal finance.)

Why are the authors dismissive of saving rate? Their research shows that for each 1% bump in saving rate over thirty years, a person can expect a 2.16% increase in standard of living at retirement — assuming a 0% real return. This same increase could be achieved by working an extra 3.3 months past target retirement age.

But what if instead of assuming a 0% real return on investment, we assume a 7% real return on investment (which is close to the long-term return of stocks)? Then each 1% increase in saving rate over thirty years leads to a 4.79% increase of standard of living during retirement. In this case, it would take six months of extra work to match a 1% jump in saving rate.

I think the authors are far too quick saving rate in favor of working longer. They’re working with tiny, tiny fractions. Instead of talking about a 1% increase to savings, why not talk about something meaningful, such as a 10% or 20% increase to saving rate?

Assuming average stock-market returns (instead of 0% returns) — where every 1% increase to savings is equivalent to six months of extra work — then we find that by boosting your saving rate for 10% over thirty years means you can retire five years earlier. If you boost your saving rate by 20%, you can retire ten years earlier. These are significant amounts of time!

To summarize, this article gives us two new financial rules of thumb. First, for each year you work past standard retirement age, you’ll enjoy roughly a 10% increase to your post-retirement standard of living. Second, each 1% bump to your saving rate is roughly equivalent of six months you don’t have to work.

What If You Start Late?

To me, there shouldn’t be an argument about whether it’s better to work longer or to save more. Both strategies produce notable increases to standard of living in retirement. If we save more now, we’ll have more later. And if we work a little longer, that’ll provide a boost to our standard of living too.

Last of all, I’d like to point out that the authors correctly conclude that the later you start saving, the less powerful saving actually is. If you don’t begin saving for retirement until age 56, there’s far less time for the power of compounding to grow your wealth snowball. As a result, for older folks each 1% increase to saving rate is equivalent to about a month-and-a-half of extra work (as opposed to between three and six months).

This doesn’t mean that you shouldn’t start saving in your forties and fifties. It just means that the power of saving is diminished. And it means that, realistically speaking, you’ll probably have to work beyond your desired retirement age.

“How can you measure, and verify, a financial adviser’s performance for the sake of comparing one prospective adviser to another?”

While this is a common question for people to ask, it’s not really a useful way to evaluate a financial advisor — for a few reasons.

First, an advisor doesn’t recommend the same portfolio to everybody. The investment portfolio that is appropriate for you as a client may be wholly inappropriate for another client with very different circumstances.

If an advisor or advisory firm were to calculate something like the average annualized return earned by their clients over a given period, that figure wouldn’t provide a meaningful point of comparison to another advisor’s such figure. For example, if one advisor has a clientele that is primarily middle class retirees, while another advisor’s clientele is primarily super-high-earners in their 30s or 40s, the clients of the first advisor would probably have, on average, lower returns over the last several years than clients of the second advisor — and that would simply be the result of the first advisor recommending appropriately low-risk portfolios for his/her clients.

In short, there’s no single figure that can be calculated to meaningfully measure how well the investment recommendations of a given financial advisor have performed over a given period.

Second, an advisor shouldn’t really be trying to do anything clever with respect to client portfolios. If an advisor is putting together a portfolio for you, a simple, boring portfolio of index funds/ETFs that approximately match the market’s return is your best bet. Intentionally seeking out an advisor who shows you a backtested, market-beating portfolio is setting yourself up for disappointment.

Finally, an advisor who engages in actual financial planning does a whole lot more than just make investment recommendations for clients.

A financial planner can also provide advice about tax planning or estate planning. They can help you evaluate your insurance coverage to see if there’s anything important you have missed (e.g., disability insurance). They can help with Social Security planning, and retirement planning in general. They can provide assistance with budgeting if that’s something you struggle with. They can provide advice with regard to your employee benefit options (e.g., help determine which health insurance is the best fit for your family).

And frankly, investment management is quickly becoming the least valuable part of financial planning. While there are still plenty of people whose investment performance would be improved by working with a financial advisor, the list of tools available for DIY investors to create a low-maintenance portfolio has grown dramatically over the last decade. Investors can now choose from Vanguard’s LifeStrategy funds, low-cost indexed target retirement funds at various providers, a smorgasbord of total market index funds/ETFs, or low-cost services like Betterment or Vanguard Personal Advisor Services.

What is the Best Age to Claim Social Security?

Read the answers to this question and several other Social Security questions in my latest book:

Social Security Made Simple: Social Security Retirement Benefits and Related Planning Topics Explained in 100 Pages or Less

Disclaimer:Your subscription to this blog does not create a CPA-client or other professional services relationship between you and Mike Piper or between you and Simple Subjects, LLC. By subscribing, you explicitly agree not to hold Mike Piper or Simple Subjects, LLC liable in any way for damages arising from decisions you make based on the information available herein. Neither Mike Piper nor Simple Subjects, LLC makes any warranty as to the accuracy of any information contained in this communication. I am not a financial or investment advisor, and the information contained herein is for informational and entertainment purposes only and does not constitute financial advice. On financial matters for which assistance is needed, I strongly urge you to meet with a professional advisor who (unlike me) has a professional relationship with you and who (again, unlike me) knows the relevant details of your situation.

You may unsubscribe at any time by clicking the link at the bottom of this email (or by removing this RSS feed from your feed reader if you have subscribed via a feed reader).

Last week, Ben Carlson from A Wealth of Common Sense published an interesting article about how staying rich is harder than getting rich . H...

Research shows over 50% of Americans will find themselves in the top 10% of earners for at least one year of their lives. More than 11% will find themselves in the top 1% of income-earners at some point. And close to 99% of those who make it into the top 1% of earners will find themselves on the outside looking in within a decade.

It’s great that so many people get to taste what it’s like to earn a lot of money, if only for a little while. What’s not so great is that as most people earn more, they spend more. But if you spend all (or most) of what you earn as you’re surfing an income bubble, you can find yourself in trouble when that bubble bursts.

Carlson quotes a story about a couple that lived a lavish lifestyle because they were making a lot of money. When the income dried up, they realized they had nothing left. They were broke. Says the husband: “The money was just coming so fast and so easy that my ego led me to believe that, ‘Oh, this is my life forever.'”

I’ve been thinking about that last line for a week now: “This is my life forever.” This couple fell for a common (but seldom examined) mental trap: the forever fallacy. The forever fallacy is the mistaken belief that you will always have what you have today, that you’ll always be who you are today.

The Forever Fallacy

It’s easiest to see the forever fallacy at play in extreme cases. Take professional athletes, for instance.

In a 2009 Sports Illustrated article about how and why athletes go broke, Pablo S. Torre wrote that after two years of retirement, “78% of former NFL players have gone bankrupt or are under financial stress.” Within five years of retirement, roughly 60% of former NBA players are in similar positions.

Fundamentally, the problem here is the forever fallacy. Athletes (and popular entertainers) tend to enjoy a few years during which they earn great gobs of money. The challenge is to figure out how to make five years of income last for fifty years. This never occurs to most of them. As the money is rolling in, it feels like the money will always be rolling in. When the income stops, the pain begins.

“[A pro athlete] can’t live like a king forever,” says Bart Scott in ESPN’s Broke, a documentary about pro athletes and their money problems. “But you can live like a prince forever.”

The forever fallacy doesn’t just trap athletes and entertainers and lottery winners. It snares average folks like you and me too.

I’m sure we’ve all had friends who found themselves flush, whether from a windfall or from a raise at work. They succumb to lifestyle inflation, spending more as they earn more. They buy a bigger house, a new car, a boat. Then, without warning, something awful occurs and they’re no longer rolling in dough. It felt like the good times would last forever — but they didn’t.

The forever fallacy manifests itself in lots of little ways too.

When you choose not to keep an emergency fund because you’ve never needed one in the past, you’re succumbing to the forever fallacy.

When you take out a large mortgage, one that pushes the limits of your earning power, you’re giving in to the forever fallacy.

When you fund your lifestyle through debt, you’re living in the forever fallacy.

The forever fallacy doesn’t apply only to positive expectations. People also give in to the forever fallacy with negative expectations. They’re trapped in a minimum wage job and project that they’ll always be working minimum wage. They’re in a shitty marriage and let themselves believe that they’ll always be trapped in a shitty marriage. And so on.

The key thing to understand is that everything changes. You change. Your circumstances change. The people around you change. Nothing is forever. The challenge then is to balance this concept — everything changes — with living in the present. You must learn to enjoy today while simultaneously preparing for possible tomorrows.

Negative Visualization

One way to protect yourself from the forever fallacy is to play “what if?” games.

In A Guide to the Good Life by William Irvine, the author advocates a psychological exercise he calls “negative visualization”. Learn to ask yourself, “What’s the worst that could happen?”

The Stoics…recommended that we spend time imagining that we have lost the things we value — that our wife has left us, our car was stolen, or we lost our job. Doing this, the Stoics thought, will make us value our wife, our car, and our job more than we otherwise would.

Sounds a little gloomy, right? Irvine says that’s not the case. You’re not meant to dwell on these things, but to occasionally ponder them as a thought exercise.

In my own life, I used to imagine what it would be like if I lost my job. “I could always go to work at McDonald’s,” I thought. “And I grew up in a run-down trailer house. Worst case, I could always live in something like that again.” This line of thinking drove my ex-wife crazy but gave me comfort. I knew that if disaster struck, I’d be fine flipping burgers and living in a trailer park. I’ve done it before and can do it again.

Nowadays I challenge myself by thinking about what might happen if the stock market crashed or our house burned down. What would I do if I lost everything? Where would I go? How would I earn money?

The Stoics took this exercise even further. Seneca the Younger encouraged followers to live as if each moment were their last. But that’s not to say that he wanted people to descend into debauchery. Here’s how Irvine explains it:

Living as if each day were our last is simply an extension of the negative visualization technique: As we go about our day, we should periodically pause to reflect on the fact that we will not live forever and therefor that this day could be our last. Such reflection, rather than converting us into hedonists, will make us appreciate how wonderful it is that we are alive and have the opportunity to fill this day with activity. This in turn will make it less likely that we will squander our days.

Negative visualization is useful because it forces you to look beyond the here and now, to imagine other possible realities. It encourages you to consider that the future might not be a linear projection of the present. I think it can also help nudge a person to think about what’s truly important in their life.

Too many people squander their days and their dollars. They spend their time and money on things that don’t matter, not even a little. When you die, will you be glad you watched every episode of Game of Thrones? Or will you regret not having used that time for something better aligned with your passion and purpose?

Be Prepared

Perhaps the best way to protect yourself from the forever fallacy is to become proactive. Like a Boy Scout or a Girl Guide, be prepared to “do the right thing at the right moment”.

In the realm of personal finance, there are plenty of things you can do to be prepared.

Get out of debt and stay out of debt. As somebody who was deep in debt for almost twenty years, I now see that carrying debt is a classic expression of the forever fallacy. It’s blind faith that you’ll be able to repay what you owe in the future.

Maintain an emergency fund to handle unexpected problems such as car accidents and broken bones.

Start an opportunity fund so that you can take advantage of the unexpected good things that come along, such as a chance to travel with friends or a great deal on a used pickup truck.

Carry adequate insurance to protect yourself from catastrophic loss like earthquake, heart attack, or giant fire-breathing monsters from the sea.

Boost your saving rate, the gap between what you earn and what you spend. This has a two-fold effect. A high saving rate helps you set aside more for the future, but it also makes you more resistent to the slings and arrows of outrageous fortune today.

Build social capital by creating a web of friends, family, and colleagues that you trust and support — and who trust and support you.

The truth is you’re never going to beat the forever fallacy and neither am I. Not completely, anyhow. It’s simply human nature to extrapolate our present and past into the future. The best we can do is mitigate the trouble caused by this tendency.

Be Like Bond

Recently, I’ve been reading the original James Bond novels by Ian Fleming. I like the books because the literary Bond is more realistic than the cinematic Bond; he’s less of a superhero and more of an everyday person (who happens to be a secret agent). He eats too much, drinks too much, and can be a bit lazy at times.

Where Bond excels, however, is preparation. He’s always thinking a move or two ahead of his foes. He tries to anticipate what might go wrong so that he can take steps to prevent trouble. This doesn’t mean that he always evades trouble — there’d be no drama if he did — but his dedication to preparation helps him avoid some scrapes while also allowing him to sometimes survive certain death.

Bond does not suffer from the forever fallacy, neither in the short term nor the long. (He often wonders if he’s near the end of his career, too old to continue working as a spy.) We’d all have greater success in life if we were more like James Bond, if we took precautions, if we didn’t give in to the forever fallacy.

Over the next few weeks at Get Rich Slowly, I plan to ramp up the production level once again. I’m not going to return to the pace of one article per day that I was maintaining at the start of the year, but I’m not going to rest at two articles per week like I did in June, either. I’m guessing we’ll end up at three to four articles per week.

To start, here’s some raw video from Miami Beach, Florida in which three men work together to distract a convenience store clerk in order to install a card skimmer at a point-of-purchase card reader.

This is interesting to me because I’ve never understood how these things work. I don’t know how to spot card skimmers, and I don’t know how crooks install them.

Well, apparently it takes like two seconds for them to install the device — and they look (superficially, at least) exactly like the regular card readers. That sucks. I don’t know how to avoid a skimmer, and I don’t know what to tell you in order to make sure that you’re safe.

Here are two articles about card skimmers (and how to protect yourself):

Card skimming is relatively uncommon but it does happen. Your best bet — as it is in many situations like this — is to check your bank accounts regularly to be sure there’s no suspicious activity.

I’m beginning to suspect that this is what’s been happening to Kim when she gets her debit card info stolen. I’ll bet it’s not some sort of elaborate scam or mail-theft ring. I’d wager that someplace she frequents regularly has had an issue with scammers installing card skimmers.

The “three-fund portfolio” (subject of a long-running discussion thread on the Bogleheads forum) is made up of three index funds: a total US stock market index fund, a total international stock index fund, and a total bond market index fund. With just three holdings, it manages to be far simpler than most people’s portfolios, while also being extremely diversified (including thousands of stocks from around the world, as well as thousands of bonds).

Larimore’s new book is very brief — in the spirit of Bill Bernstein’s If You Can. For those who are already well versed in the Bogleheads literature (e.g., having already read the original Bogleheads Guide to Investing, and other books by Bernstein, Roth, Ferri, etc.) the book will be unlikely to provide new information, but it will likely be an enjoyable read nonetheless, as it was for me. (I always enjoy reading about Taylor’s lessons accumulated via many years of experience.)

I think where the book will really shine is as a gift for new investors. Because of the book’s brevity (easy to read in an afternoon), it is more likely to actually be read than the typical book about investing. And because of the book’s singular focus, it will be easy for new investors to internalize the message.

Disclaimer:Your subscription to this blog does not create a CPA-client or other professional services relationship between you and Mike Piper or between you and Simple Subjects, LLC. By subscribing, you explicitly agree not to hold Mike Piper or Simple Subjects, LLC liable in any way for damages arising from decisions you make based on the information available herein. Neither Mike Piper nor Simple Subjects, LLC makes any warranty as to the accuracy of any information contained in this communication. I am not a financial or investment advisor, and the information contained herein is for informational and entertainment purposes only and does not constitute financial advice. On financial matters for which assistance is needed, I strongly urge you to meet with a professional advisor who (unlike me) has a professional relationship with you and who (again, unlike me) knows the relevant details of your situation.

You may unsubscribe at any time by clicking the link at the bottom of this email (or by removing this RSS feed from your feed reader if you have subscribed via a feed reader).

Every Tuesday and Thursday morning for the past four weeks, I’ve awakened early and driven to the gym for a one-hour workout with a personal...

Every Tuesday and Thursday morning for the past four weeks, I’ve awakened early and driven to the gym for a one-hour workout with a personal trainer. This is awesome but it also sucks.

Why does it suck? Because:

I am old.

I am fat.

I am out of shape.

Plus, who likes getting up at five o’clock? Not me! I can handle 6:30 no problem (and left to my own devices, that’s when I’ll naturally rise) but crawling out of bed ninety minutes earlier destroys me.

At the same time, this change has been awesome. Eight years ago, when I was at the heaviest weight of my life, I forced myself to get up early and go to the local Crossfit gym. After two years, I’d left peak fatness behind and achieved peak fitness. I was in the best shape of my life! Now I have a long way to before I get back to that point, but the key is that I’ve started.

Aside from improving my physical fitness (I’ve noticed positive changes already), this move has improved my mental fitness. Honestly, that’s actually what prompted me to get back to the gym. After admitting to myself that my depression was messing up my life, I resolved to make changes.

At first, I wanted some magic instant cure for the depression. There isn’t one. As with most things in life, there are no shortcuts to solving mental illness. (Perhaps a pill might be considered a shortcut, but pills come with side effects.) To get better, I need to do the things I know help me fight the disease.

Chief among these cures is fitness. When I’m active and fit, my mental state is much better than when I’m fat and sedentary.

I’m taking other steps too, of course. I’ve been spending more time with friends. And I’ve come to the realization that my sleep has been a huge culprit these past few months. I’ve been getting shitty sleep due to my weight and alcohol consumption. So, I’m (once again) working to reduce the alcohol, and I did an in-home sleep study that revealed my sleep apnea has returned. I’m waiting for a mouth-guard to be manufactured, which should improve my sleep quality.

Notice that none of these things are shortcuts. Drinking less, eating better, exercising more, and addressing my sleep issues all take time, money, and effort. I can’t beat the depression by simply wishing it away. Thinking about getting better will solve nothing. Only action matters.

Magical Thinking

This morning while my trainer was leading me through proper form on the push press, he talked to me about his current financial situation. He just lost a few hours at another gym, and it’s putting the pinch on his budget. (Cody also happens to be one of my best friends, which is why he was sharing this info.)

“So, I applied for a new job,” Cody said. “It’s something completely different. It’s an online sales position. I met a gal the other day who’s doing the same thing and she made $9000 last month while working only twenty hours per week!”

“That’s great,” I said. “It’d be awesome if you got the position.” Then the conversation turned to the motorcycle trip we’re taking next weekend. Which route should we take from Portland to central Oregon? Where should we stop? What should we do?

Later, though, I got to thinking. While it is awesome that Cody has applied for this new job and I hope he gets it, I worry that he’s exhibiting what I call “magical thinking”. Instead of pursuing mundane work in a field he knows (and is good at!), he’s looking for a shortcut. That shortcut is a high-paying job in an area he knows nothing about.

This is the sort of thing I used to do all of the time. Back when I was deep in debt, I was always looking for shortcuts. Instead of doing what I knew needed to be done, I was constantly searching for ways to get rich quickly.

Just the other day, I found an example of the sort of shortcut I used to be drawn to. In the mid-1990s, I read an ad in a magazine about how you could make big bucks just by reading books. Holy cats! I liked reading books. I sent away for info. In return, I got this pamphlet that promised publishers would pay me $100 (or more) for every book I read:

I can’t recall if I tried to follow the pamphlet’s advice or not. I suspect “not”. It took effort. I didn’t want to solve my problem by exerting effort. I wanted it to magically go away. I wanted a shortcut to success, a shortcut to debt elimination.

“Money is a game,” Douglas said at the start of our third hour. “And there are rules to the game. Some folks try to make the rules more complicated than they have to be. Others try to find ways around the rules. Still others believe the rules are a mystery, that they’re hidden and have to be uncovered. The reality is the rules to the game of money are simple. They’re not easy but they’re simple. And you already know them.”

Douglas and I walked the audience through “the rules of the game”. The final rule, which we added to the slide moments before we started the presentation, was this: There are no shortcuts.

If I want to beat my depression, I have to get fit. I have to eat right. I have to drink less. I have to spend time with friends. And so on.

If you want to achieve your financial goals, you have to spend less than you earn — you need a positive saving rate. That’s how the math works.

If you want to earn more, you have to do the things that lead to greater income: ask for a raise, work a second job, change careers.

If you want to spend less, you have to find ways to reduce your consumption: choose a cheaper home, drive less, limit your luxuries.

If you’ve begun to set aside savings and want to create a wealth snowball, you have to invest wisely and you need to be patient. There’s no magic investment that’s going to turn your $1000 into $100,000 in less than a year.

As a life-long shortcut seeker, I completely understand the appeal of magical thinking. It took me months to realize that’s the approach I was taking to defeating my depression. I was doing nothing and hoping that things would simply turn around on their own. But you know what? Things never turn around on their own. (If they do, the improvement is coincidental and generally short-lived.)

There are no shortcuts.

If you want to achieve anything in life — whether it’s getting out of debt, writing a book, or shedding your beer belly — you have to put in the work necessary to make it happen. That’s not what people like me want to hear but it’s the truth. The good news is that, as with the game of money, the answers are usually simple — even if they’re not easy.

Footnote: While finishing this article, I realized that many of the spam comments I deal with are targeted at folks looking for shortcuts. Here’s a typical example:

“Click this link and watch all of your troubles wash away.” That’s the very definition of magical thinking.

“I’ve been reading about the safety first school of retirement planning because I think that appeals to me more than the probability method of just spending from risky investments and assuming everything will ‘probably’ be okay. My question is how to start putting such a plan into action in advance.

With the old school probability method, I would just keep building my mutual fund holdings, possibly rebalancing to hold more bonds instead of stocks. The ‘safety first’ method focuses on delaying social security or buying an annuity. But I can’t delay social security until I’m 62. And I can’t, or shouldn’t, buy an annuity in my 50’s either. So what should I, as a safety first investor in my 50’s, be doing right now in the years leading up to retirement?”

As a bit of background for readers unfamiliar with the terms, there are two broad schools of thought with regard to retirement planning. The first school of thought plans to finance retirement spending primarily via liquidating a mutual fund portfolio (or a portfolio of individual stocks/bonds) over time. This approach relies heavily on historical studies and/or Monte Carlo simulations to calculate how safe a certain level of spending is, given various assumptions. This approach is sometimes referred to as the “probability” school of thought, because it focuses on metrics such as “probability of portfolio depletion.”

The second approach essentially says, “I don’t want to bet my retirement on the validity of such studies/assumptions. I’d rather lock in sufficient safe income (e.g., via annuities, pension, Social Security) to satisfy my needs and only use mutual funds to finance my discretionary spending.” This school of thought it sometimes referred to as the “safety first” or “safe floor” method of retirement planning.

The answer to the reader’s question about how to start implementing a “safety first” plan in advance is that you start building a TIPS ladder (or other bond ladder, or CD ladder) that you will use to fund your spending while you delay Social Security, or to fund your annuity purchase.

To plan in advance for delaying Social Security, you would allocate a portion of the portfolio to a bond ladder that will provide the necessary cash each year for 8 years. For example, if you’re passing up $1,500 per month ($18,000 per year) for 8 years, you could start building an 8-year bond ladder, with roughly $18,000 maturing each year.

If Social Security at age 70 still doesn’t give you a sufficient “safe floor” of income to meet your needs/satisfy your risk tolerance, then you should start thinking about a lifetime annuity.

To start planning in advance for an annuity purchase, you’d do something similar — build up bond holdings that you would eventually use to fund the purchase. What’s different about this, relative to delaying Social Security, is that you don’t know how much the annuity will cost. For example, if you anticipate buying a lifetime annuity at age 70 that pays $10,000 per year, there’s no way to know right now (in your 50s) how much that annuity will cost, because you don’t know how high or low interest rates will be when you turn 70.

The solution, rather than buying a bunch of bonds that mature when you turn 70, would be to work on building bond holdings that, when you turn 70, will still have a duration roughly equal to that of the annuity you expect to purchase. This way, the market value of your bonds will rise/fall along with the cost of such an annuity, helping to offset the interest rate risk that you face with the annuity purchase. (Here’s a great Bogleheads thread on that topic.)

What is the Best Age to Claim Social Security?

Read the answers to this question and several other Social Security questions in my latest book:

Social Security Made Simple: Social Security Retirement Benefits and Related Planning Topics Explained in 100 Pages or Less

Disclaimer:Your subscription to this blog does not create a CPA-client or other professional services relationship between you and Mike Piper or between you and Simple Subjects, LLC. By subscribing, you explicitly agree not to hold Mike Piper or Simple Subjects, LLC liable in any way for damages arising from decisions you make based on the information available herein. Neither Mike Piper nor Simple Subjects, LLC makes any warranty as to the accuracy of any information contained in this communication. I am not a financial or investment advisor, and the information contained herein is for informational and entertainment purposes only and does not constitute financial advice. On financial matters for which assistance is needed, I strongly urge you to meet with a professional advisor who (unlike me) has a professional relationship with you and who (again, unlike me) knows the relevant details of your situation.

You may unsubscribe at any time by clicking the link at the bottom of this email (or by removing this RSS feed from your feed reader if you have subscribed via a feed reader).

Two years ago today, Kim and I returned to Portland after fifteen months traveling the United States in an RV. Believe it or not, I’ve never...

Two years ago today, Kim and I returned to Portland after fifteen months traveling the United States in an RV. Believe it or not, I’ve never published an article about the trip and how much it cost. Although we kept a travel blog for most of the adventure (including a page that documented are expenses), I’ve never gathered everything into one place. Until now.

Today, I want to share just how much we spent on the journey — and some of our favorite stops along the way. It seems like the perfect post to celebrate the start of summer, don’t you think?

The Lure of Adventure

All my life, I’ve wanted to take a roadtrip across the United States.

When I was young, I was lured by the adventure. I wanted to climb mountains, swim rivers, and explore canyons. The older I got, the more fascinated I became by the country’s regional differences. The U.S. is huge, a fact that most foreign visitors forget. Most American citizens don’t even realize how big the country is. I wanted to see and experience it all.

Although I’ve dreamed of a cross-country roadtrip, it’s never been practical. As a boy, my family was poor. My parents didn’t have money for something like this. As a young adult, I couldn’t afford it either. For a long time, I was deep in debt. Besides, where would I find the time? I had to work! To top things off, my wife had zero interest in driving cross country.

But in my forties, a curious set of circumstances came together to move my epic roadtrip from dream to reality.

I sold Get Rich Slowly, which meant I suddenly had a surplus of both time and money.

My wife and I got a divorce. When I began dating again, I chose a partner whose adventurous spirit surpassed my own.

One day in early 2014, my girlfriend Kim asked me out of the blue, “What do you think about taking a cross-country roadtrip?”

As Kim and I began to discuss this adventure, our biggest concern was money. As a financial writer, I’m acutely aware that every dollar I spend today is roughly equivalent to seven dollars I could have in retirement. Every day, I preach the power of saving. I wanted to keep our trip as cost-effective as possible. (Besides, Kim would have to quit her job as a dental hygienist in order to travel — a huge financial sacrifice.)

My goal was to keep our costs under $50 per person per day. In fact, I had high hopes we could do the trip for $33 per person per day (for a total of $24,000). But the U.S. is expensive. How could Kim and I make this happen?

From the start, we knew hotels were out. Even cheap lodging would be far too expensive for us to stay within budget. Personally, I liked the idea of bicycling across the country like my friends Dakota and Chelsea have done. Kim wasn’t keen on the idea. (Nor was she willing to make the trip by motorcycle despite being a die-hard Harley girl.)

After a lot of research, and after talking with Chris and Cherie from Technomadia, I came to a conclusion: The best balance of cost and comfort would come from crossing the country in an RV. With this bare outline of a plan, the true trip prep began.

Searching for Bigfoot

After deciding to travel by RV, there were more questions to answer. Neither of us had experience with recreational vehicles. Among other things, we needed to figure out:

Should we buy a truck and a trailer?

Would it be better to buy a motorhome and tow my 2004 Mini Cooper?

What about new or used? With used, you never know what you’re getting. But a new RV costs $80,000 or more — and loses value quickly.

How much space did we need? What kinds of amenities?

After crunching the numbers, there was an obvious “best choice” for us. If we bought a used motorhome, we could tow a car we already owned while (we hoped) avoiding a big hit from depreciation. In fact, if we were diligent every step of the way, it might even be possible to resell our RV after the trip and recoup most of what we’d paid for it!

We spent the autumn of 2014 patiently sifting through Craigslist ads for used motorhomes. We visited dealerships. We attended the local RV Expo. We walked through dozens of models searching for the right fit. Some were too long. Some were too short. Some were too fancy. Many were run-down and in a state of disrepair.

Finally, in early January 2015, we found the perfect rig: a 2005 Bigfoot 30MH29RQ. (Translation: A 29-foot motorhome with a queen bed in the rear.) The owner wanted $38,000 for it — a fair price. He wouldn’t budge when I tried to negotiate, but I was okay with that. My research revealed he was actually selling a slightly better model, one worth a few thousand dollars more than he was asking. We bought it.

Over the next two months, Kim and I prepped Bigfoot for departure. We spent $2000 making minor repairs and installing a towbar on the Mini Cooper. We cleaned the motorhome from top to bottom. We took weekend test trips to RV parks around Oregon and Washington. When all was said and done, we’d invested $40,000 to get our caravan ready for the road.

Into the West

Kim and I left Portland on the morning of 25 March 2015, my forty-sixth birthday. We sped through Oregon — we love the state, but we’re both familiar with it — and entered northern California. We spent our first week on the road exploring the Redwoods and weaving through wine country.

Along the way, we got a crash course in driving a motorhome.

Near Cloverdale, California we took a wrong turn onto a cliff-side gravel road. We stopped immediately. Good thing, too. Turns out a week earlier some other poor soul had driven his RV over the side of the cliff. East of Sacramento, we took another wrong turn and found ourselves driving down a narrow dike road during rush hour while high winds buffeted the RV. Very scary.

At times we felt like Lucy and Desi in The Long, Long Trailer, but after a couple of weeks Kim and I had learned how to handle our motorhome, both on the road and off.

Early in the trip, our expenses were out of sight. We ate out too often. We bought too much wine. We did too many touristy things without searching for discounts. We rationalized that since we were visiting all of these new places (and might never return), we might as well pay to experience them to the fullest. This was a once-in-a-lifetime adventure, after all.

The problem, of course, was that lots of fun costs lots of money. Ten days into the trip, our average spending was over $120 per day (or over $60 per person per day) — almost twice what we’d hoped to spend. Yikes!

We tightened the purse strings. We stopped eating out so much and cooked in the motorhome. (We cook a lot at home normally, so this wasn’t a tough transition.) We bought a National Parks pass, perhaps the best purchase of our entire trip. (For an $80 one-time fee, you get one year of unlimited access to all sorts of government-owned sites.) We learned to entertain ourselves at night with books and boardgames and a hard drive filled with old movies — and an iPad filled with comic books.

During our 33 days in California, we marveled at the state’s vast variety of terrain. We drove through forests and deserts, skirted ocean cliffsides and walked across mountain streams. We hated L.A. traffic — not recommended when you’re in a motorhome towing a car — but enjoyed almost everything else.

We loved Arizona even more. Maybe we had low expectations, but we were blown away by the magnificent scenery of the Grand Canyon state. For nineteen days, we basked in the warm spring sun and admired the colorful rock formations.

It was in Arizona that we discovered the joys of drycamping (or “boondocking”). For the first seven weeks of our trip, we mostly stayed in RV parks and campgrounds. At $20 to $50 per night (with the average park costs around $35), lodging was our biggest expense — by far. Drycamping costs nothing. All you do is find a spot where you can legally park for the night — National Forest land, a friend’s driveway, certain businesses and casinos — and set up camp. You don’t have access to electricity or fresh water, but that’s okay. The beauty of an RV is that it’s self-contained. (Our Bigfoot had a generator for electricity and a 63-gallon freshwater tank.)

After boondocking only once during our first 50 days on the road, we managed to live off the grid for 33 of the next 80 nights.

Once we began pinching pennies, our travel costs plummeted. We weren’t spending $120 per day anymore. Our average daily spending fell to $50, which lowered the trip average to about $80 per day.

A Costly Repair

With all this frugality, did we feel like we were depriving ourselves? Not at all! As we made our way from Arizona to Utah to Colorado, we found we could still afford wine and an occasional restaurant meal. Plus, we were paying to do a lot of touristy things, such as soak in the hot springs in Ouray and ride the narrow-gauge train from Durango to Silverton.

At the end of May, we stopped for a week to visit family and friends near Denver. During this break, our RV costs dropped to zero — no fuel or lodging expenses while we stayed with Kim’s mother and hung out with Mr. Money Mustache — which allowed us to spend a little more on fun. Good thing too because Fort Collins has a great beer scene.

We hit the road again in early June, making our way into Wyoming to visit Yellowstone and the Tetons. We zipped over to Idaho to spend time with Kim’s father in Sun Valley. From there, we drove north into Montana to lounge around Flathead Lake and explore Glacier National Park. Costs stayed low as we crossed Montana to enter the beautiful Black Hills of South Dakota.

After celebrating Independence Day in Deadwood, our average daily spending for the trip was about $84. We felt good about that number. It’d be nice if it were lower, but $42 per day per person seemed reasonable. At that rate, the trip would cost us $30,000 for the entire year.

On July 8th, the tenor of our trip changed. So did our costs. We were cruising across the vast emptiness of central South Dakota when the motorhome’s engine overheated. We pulled off to give it a rest. The oil level looked fine, but I added more just in case. It didn’t help. An hour down the highway, the engine seized up completely. Turns out Bigfoot had “spun a bearing” and the engine was toast. (Also turns out that spun bearings are not uncommon with this particular engine.)

Unfortunately, we were in the middle of nowhere. The nearest town was Plankinton, South Dakota (population 707). Fortunately, the folks in Plankinton were friendly. The owners of the local garage diagnosed the problem and ordered parts. Meanwhile, we got to know the owners of the only RV park in town. We spent ten days drinking beer with Plankintonians while exploring nearby attractions such as the Corn Palace and the real-life homestead of Laura Ingalls Wilder.

In the end, the engine repair cost $7751.39. Ouch! We did not count this against our daily trip budget but instead factored it into our overhead, much like we had with the purchase price of the RV. (You might choose to account for it differently.)

The Expensive East

When the new engine was ready, we waved good-bye to our new friends in Plankinton. We drove through Minnesota to Wisconsin, where we spent a week in the Great North Woods. (At the recommendation of world traveler Gary Arndt, whom we had lunch with near Milwaukee, we took a boat ride out to view the amazing Apostle Islands.)

After eating our fill of Wisconsin cheese, we crossed into Michigan’s upper peninsula and then drove south to Indiana’s Amish country, where we rested for a week. (We also took the time to dart into Chicago for an overnight trip.) From there, we moved to Indianapolis and Cincinnati.

As we made our way east, we noticed some interesting changes.